Missouri Medicaid planning in 2026 means protecting your home, your savings, and your spouse from nursing home costs that can reach $9,000 a month before you’ve had time to breathe. After 27 years of helping Missouri and Arkansas families through exactly this, I can tell you one thing with confidence: the families who plan ahead keep what they built. The ones who wait until a health crisis hits? They lose options fast. MO HealthNet has strict asset limits, a 60-month lookback period, and an estate recovery program that comes knocking after death.

Let’s talk about what actually matters for Missouri Medicaid planning in 2026.

Missouri’s nursing home Medicaid asset limit dropped to $6,068.80 on July 1, 2025. If you have not checked your exposure against that number, now is the time.

The five-year lookback period does not forgive good intentions. Every unplanned asset transfer is a potential penalty period.

Your home is safe during your lifetime on Medicaid. It is not safe from estate recovery after death without the right trust structure in place.

A revocable living trust protects you from probate. It does nothing against Medicaid spend-down or estate recovery.

Missouri and Arkansas play by different rules. A strategy built for one state can fail badly in the other.

The One Big Beautiful Bill Act cut $911 billion from federal Medicaid over ten years. Home and community based services are the most vulnerable piece of that picture.

The families who protect the most are the ones who planned the earliest. Starting the five-year clock today costs nothing compared to what waiting costs later.

What Missouri’s 2026 Medicaid Numbers Mean for Your Family

The Asset Limit That Catches Most Single Applicants Off Guard

Missouri’s countable assetlimit is $6,068.80 for a single nursing home Medicaid applicant, effective July 1, 2025. That means MO HealthNet expects you to spend down nearly everything before coverage kicks in. Your home, one vehicle, and personal belongings are exempt assets, but your savings, investments, and most financial accounts are not.

How the Community Spouse Resource Allowance of $162,660 Works in Practice

Spousal impoverishment rules exist specifically so the healthy spouse at home does not end up broke. In Missouri, the community spouse can keepup to $162,660 in countable assets in 2026. This protection, called the Community Spouse Resource Allowance, is one of the most valuable tools in Medicaid planning, and most families never hear about it until after a crisis hits.

A retired schoolteacher in her early seventies came in after her husband entered a memory care facility. She assumed she would have to spend their entire joint savings down to almost nothing. Once we walked through the spousal impoverishment standards together, she learned she could protect the full $162,660 allowance, keep the house, and still qualify her husband for nursing home Medicaid. The relief on her face said everything.

Income Caps, the Monthly Maintenance Needs Allowance, and What Gets Left Over

Missouri’s nursing home Medicaid income limitsits at $2,982 per month for 2026. For married couples, the Monthly Maintenance Needs Allowance protects a minimum of $2,644 per month for the community spouse’s living expenses. According toKFF’s May 2025 Missouri Medicaid fact sheet, people aged 65 and older account for 60% of all MO HealthNet spending despite being just 24% of enrollees, which tells you exactly how significant long-term care costs are in this state.

Table: Missouri vs. Arkansas Medicaid Planning (2026)

Planning Factor

Missouri (MO HealthNet)

Arkansas Medicaid

Single Applicant Asset Limit

$6,068.80

$2,000

Nursing Home Income Limit

$2,982/month

$2,982/month (income cap state)

Excess Income Solution

Not required

Qualified Income Trust (Miller Trust)

Transfer Penalty Divisor

$7,909/month

~$6,083/month

Community Spouse Asset Allowance

$162,660

$137,400

Home Equity Interest Limit

$752,000

$752,000

Estate Recovery Scope

Broad (probate and some non-probate)

Probate estate

Lookback Period

60 months

60 months

Revocable Trust Protection

None

None

MAPT Effectiveness

Strong

Strong

Key Application Body

Missouri Dept. of Social Services

Arkansas DHS

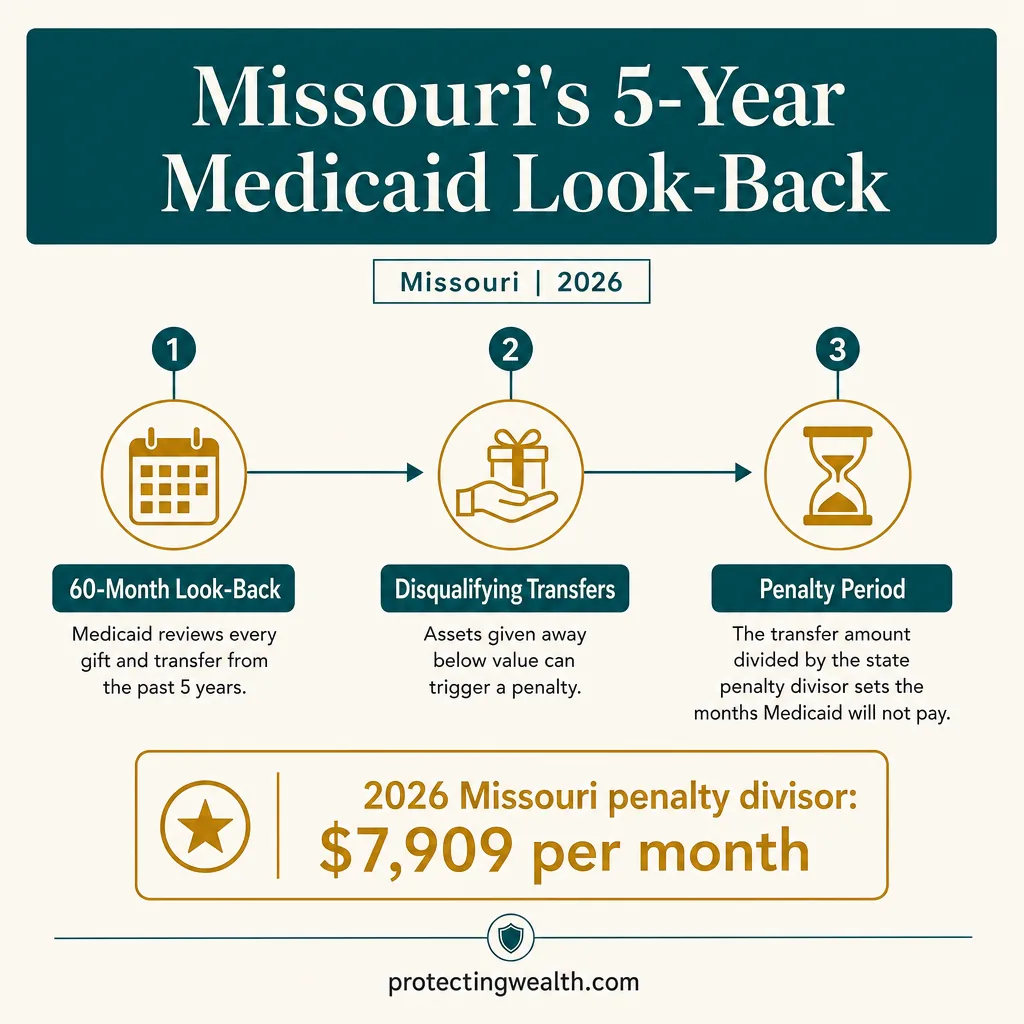

How Missouri’s five-year Medicaid look-back works (Missouri, 2026).

The Five-Year Look-Back Rule Is Not What Most Missouri Families Think It Is

What Missouri Medicaid Reviews During Those 60 Months

When you apply for nursing home Medicaid in Missouri, the Missouri Department of Social Services looks back through every financial transaction you made in the 60 months before your application date. Every gift, every transfer, every asset that left your name gets scrutinized. This is not about catching criminals. It is about confirming that you did not give away countable assets specifically to meet the Medicaid asset limit.

How the Penalty Divisor of $7,909 Turns a Gift Into Months Without Coverage

Missouri’s transfer penalty divisor is$7,909 per month in 2026. In simple words, if you gifted $79,090 to your children two years ago, Missouri divides that amount by $7,909 and assigns you a ten-month penalty period during which Medicaid will not pay for your nursing home care. You are still expected to pay that bill yourself. I have seen families face five-figure monthly invoices because of a gift they made years earlier without any guidance.

The Transfers That Are Legally Exempt and the Ones That Are Not

Not every transfer triggers a Medicaid transfer penalty, and this is where knowing Missouri Medicaid rules makes a real financial difference. Transfers to a spouse, a blind or disabled child, or a sibling with existing equity interest in the home are generally exempt resources under federal Medicaid law. Paying fair market value for something is also fine. What gets families into trouble is gifting cash, deeding property to adult children, or making charitable donations without first understanding the lookback period consequences.

A farmer in his late sixties had been gradually transferring land parcels to his three adult sons over several years, thinking he was doing smart estate planning. By the time he needed nursing home care, those asset transfers landed squarely inside the Medicaid lookback period. The resulting penalty period was substantial, and his family had to scramble to cover the gap. Had the transfers been structured properly through irrevocable trusts or timed with the five-year clock already running, the outcome would have looked very different.

Why “Starting the Clock Early” Is the Single Most Effective Move You Can Make

According toASPE and HHS research, 70% of adults who reach age 65 will develop severe long-term care needs before they die. That statistic is not meant to scare you. It is meant to explain why Medicaid planning done today, when you are healthy, preserves every option you have. Once assets move into an irrevocable Medicaid asset protection trust, the five-year lookback clock starts ticking. Waiting until a diagnosis forces your hand means shorter runways, fewer legal tools, and far less of your lifetime savings protected.

Your Home Is Exempt Right Now But Vulnerable the Moment You Pass Away

How Missouri’s Estate Recovery Program Places Liens After Death

Missouri runs one of the broader Medicaid estate recovery programs in the country. Under Missouri Revised Statutes andSenate Bill 577, no estate involving a deceased MO HealthNet enrollee can be closed without first obtaining a release from the Missouri Medicaid Estate Recovery Program. That means the state files a claim against your probate estate after death, and your home, if it passed through probate, is fair game for reimbursement of every dollar Missouri Medicaid paid on your behalf.

The Home Equity Limit of $752,000 and When It Comes Into Play

Missouri follows the federal home equity interest limit, whichsits at $752,000 in 2026. If your home’s equity exceeds that threshold, it becomes a countable asset for Medicaid eligibility purposes, not just an estate recovery target. Most families in Joplin, Springfield, and Bentonville are well under that ceiling, so the home equity interest limit rarely blocks initial eligibility. The bigger threat for most Missouri families is what happens to that home after death, not before.

Keeping the House Is Not the Same as Protecting the House

This is the distinction I want every family to sit with for a moment. Keeping the house means Medicaid did not count it against you during the eligibility test. Protecting the house means it will actually reach your children after you are gone. Some common ways Missouri families mistakenly assume the home is protected when it is not:

Believing the home automatically passes to children because it was not counted as a countable asset during the Medicaid application process

Assuming a revocable living trust shields the home from the Missouri Medicaid Estate Recovery Program, which it does not

Deeding the home to adult children inside the Medicaid lookback period, triggering asset transfer penalties

Relying on a Transfer on Death Deed without understanding that Missouri’s estate recovery reaches certain non-probate transfers for MO HealthNet enrollees age 55 and older

A widower in his early eighties from the Bentonville area had lived in the same home for over forty years. His daughter had power of attorney and was diligent about his care. When he passed after three years on nursing home Medicaid, the family was blindsided by an estate recovery claim that nearly consumed the home’s entire equity. The house had been “safe” during his lifetime. Nobody had told them that safety evaporated at death without an irrevocable trust or other protective structure in place well before the lookback period began.

According toU.S. Census Bureau data, about 1.17 million Missouri residents were aged 65 and older in 2024, representing 18.8% of the state’s total population, above the national average. With Missouri’s senior populationprojected to exceed 20% by 2030, the number of families navigating Medicaid estate recovery questions will only grow. The time to address it is before the application, not after the funeral.

How a Medicaid Asset Protection Trust Shields What You Spent a Lifetime Building

Why a Revocable Living Trust Offers Zero Protection Here

This is probably the most common misunderstanding I encounter in consultations. A revocable living trust is a fantastic probate-avoidance tool, but it provides absolutely no protection from Medicaid spend-down requirements or estate recovery. Because you retain full control over a revocable trust, Missouri Medicaid treats every asset inside it as if it still sits in your personal name. For Medicaid asset protection, the trust must be irrevocable, and that distinction changes everything.

What Assets Can Go Into a MAPT and What Should Stay Out

A Medicaid Asset Protection Trust, sometimes called an irrevocable Medicaid asset protection trust, accepts most non-retirement assets well. Your home, investment accounts, savings, and even rental property can transfer into a properly drafted MAPT. What should generally stay out are retirement accounts like IRAs and 401(k)s, since transferring those triggers immediate tax consequences that usually outweigh the Medicaid benefit. I always tell families to think of the MAPT as a container built specifically for the assets that took the longest to accumulate.

A couple in their early sixties, both retired, had built modest but meaningful wealth over four decades, primarily through a paid-off home and steady savings. They came in not because anyone was sick, but because their neighbor had just lost nearly everything to nursing home costs. Within one planning session, we moved their home and non-retirement financial accounts into an irrevocable Medicaid asset protection trust. Five years later, when the husband needed memory care, those assets were fully protected and their children’s inheritance remained intact.

How the Trust Stops Estate Recovery From Reaching Your Children’s Inheritance

Once assets are correctly titled inside an irrevocable trust, they are no longer part of your probate estate when you pass away. The Missouri Medicaid Estate Recovery Program can only reach assets that flow through probate or certain non-probate transfers tied directly to the Medicaid recipient. Assets held inside a properly structured MAPT fall outside that reach entirely. According toKFF’s 2024 estate recovery research, over half of all states pursue estate recovery aggressively, making trust planning strategies one of the most reliable defenses available to Missouri and Arkansas families today.

Medicaid Planning in Missouri Requires a Completely Different Strategy Than Arkansas

Arkansas’s Income Cap of $2,982 Per Month and the Qualified Income Trust Solution

Arkansas is an income-cap state, which means if your gross monthly incomeexceeds $2,982 in 2026, you are categorically ineligible for nursing home Medicaid without an additional legal step. That step is a Qualified Income Trust, sometimes called a Miller Trust. The QIT funnels your excess income into a dedicated account each month, bringing your countable income under the cap and restoring your Medicaid eligibility. Missouri does not use this structure, so families with assets and income in both states need separate strategies for each.

How Arkansas Calculates Penalty Periods Using a Different Divisor Than Missouri

Missouri’s transfer penalty divisor is$7,909 per month. Arkansas uses a lower divisor, currently around $6,083 per month, which means the same asset transfer produces a longer penalty period in Arkansas than in Missouri. That is a meaningful difference when you are talking about a $100,000 gift to an adult child. I have worked with families who assumed the rules they understood in Missouri applied seamlessly in Arkansas, and that assumption cost them months of uncovered nursing home bills.

A retired retail executive in her late sixties owned property on both sides of the state line and split her time between a home in Bentonville and a cabin in Joplin. When her health declined, her family assumed one Medicaid application would cover everything. In reality, her Arkansas residency meant navigating Arkansas’s income cap, a Qualified Income Trust, and a different penalty divisor, all simultaneously. Multi-state Medicaid planning is genuinely its own specialty, and having an attorney licensed in both states made the difference between a smooth application and a denial.

What Bentonville and Northwest Arkansas Families Near the State Line Need to Know

Northwest Arkansas is one of the fastest-growing regions in the country, and its senior population is expanding just as quickly. Families in Bentonville, Rogers, and Fayetteville often have financial ties to Missouri through business ownership, retirement accounts, or property. Medicaid planning in Missouri differs from Arkansas in asset limits, penalty divisors, estate recovery scope, and income rules, so living near the state line does not mean the rules blend together. Medicaid eligibility is determined by your state of legal residence at the time of application, full stop.

Crisis Planning After a Diagnosis Is Not Impossible, But the Window Is Shorter Than You Think

Spend-Down Strategies That Are Legal and Some That Will Get You Penalized

When a diagnosis arrives and nursing home care becomes urgent, families often panic and start moving money in ways that feel logical but trigger serious Medicaid penalties. I want to be clear: legal spend-down strategies absolutely exist, and some of them work remarkably well even inside the lookback period. Spend-down approaches that are generally permitted under Missouri Medicaid rules:

Paying off a mortgage or other legitimate debt

Making home modifications for accessibility and safety

Purchasing an irrevocable prepaid funeral and burial plan

Buying a newer vehicle for the community spouse

Catching up on home repairs or improvements that have been deferred

Paying for legitimate legal and financial planning fees

Gifting cash to adult children, however, is not a legal spend-down strategy. It is a transfer that Missouri’s Medicaid eligibility test will penalize directly.

Caregiver Child Exemptions and When They Can Protect a Home Transfer

The caregiver child exemption is one of the most underused asset protection strategies in Missouri Medicaid planning, and most families have never heard of it. If an adult child lived in the parent’s home for at least two years immediately before the parent entered a nursing facility, and provided care that demonstrably delayed institutionalization, the home can transfer to that child without triggering a Medicaid transfer penalty. The documentation requirements are strict, and the two-year residency must be continuous, so this exemption requires careful planning and solid records.

A 78-year-old widower with early-stage Parkinson’s had relied on his daughter for daily care for nearly three years. She had moved into his home, reduced her own work hours, and kept meticulous notes of every medication, appointment, and assisted daily task. When his condition progressed to requiring full nursing home care, we were able to document a qualifying caregiver child exemption. The home transferred to her cleanly, without a penalty period, and without estate recovery exposure.

Using Annuities and Promissory Notes as Last-Minute Planning Tools

When crisis hits and the five-year lookback period has not been cleared, Medicaid-compliant annuities and promissory notes can convert excess countable assets into an income stream that does not disqualify the applicant. According toKFF data, over 60% of nursing facility residents nationally rely on Medicaid as their primary payer, which tells you how many families are navigating exactly this situation every day.

A Medicaid-compliant annuity must be irrevocable, non-transferable, actuarially sound, and payable to the state upon the recipient’s death. These are sophisticated tools that can go wrong quickly without proper drafting, so they are not a do-it-yourself solution.

Table: Missouri Medicaid Planning Timeline: What You Can Still Do and When

Your Situation

Time Available

Best Available Strategies

What You Risk Losing

Healthy, no diagnosis

5+ years

MAPT, irrevocable trusts, gifting with lookback cleared

Snapshot date review, CSRA calculation, income protection

Community spouse income and assets at risk

Recently made large gifts

Depends on timing

Penalty period calculation, partial cure strategies

Months of uncovered nursing home costs

Home only asset remaining

Immediate

Life estate review, MAPT assessment, transfer analysis

Home equity subject to estate recovery

Federal Medicaid Cuts Under the One Big Beautiful Bill and What They Mean for Missouri Families in 2026

Which Parts of MO HealthNet Are Most Exposed to Funding Reductions

On July 4, 2025, President Donald Trump signed the One Big Beautiful Bill Act into law. The Congressional Budget Officeestimates it will cut federal Medicaid spending by $911 billion over ten years and leave 10 million more Americans uninsured by 2034. For Missouri families, the most exposed parts of MO HealthNet are the programs that serve seniors and people with disabilities, particularly those relying on optional services that states are not federally required to maintain when funding tightens. Missourireceives $12.5 billion in federal Medicaid funding annually, covering 78% of total state Medicaid spending, so federal reductions translate directly into state-level pressure.

How Home and Community Based Services Could Be Affected Before Nursing Home Coverage

Federal law requires states to cover nursing facility care under Medicaid, but nearly all home and community based services are optional. That means when states face funding pressure from reduced federal oversight and matching rate changes, HCBS waiver programs are the first place budget cuts land, not nursing homes. Missouri’s Aged and Disabled Waiver and Structured Family Caregiving Waiver programs serve thousands of seniors who want to remain at home. Those programs sit on shakier ground today than they did before July 2025.

A 71-year-old retired teacher was receiving in-home care through Missouri’s Aged and Disabled Waiver, which allowed her to stay in her own home rather than enter a facility. Her daughter, who lived nearby, had built her entire caregiving schedule around that waiver support. When we met in late 2025 to review her overall plan, the impending federal funding changes made it clear that relying solely on the waiver without a backup asset protection strategy was genuinely risky. We updated her plan to account for both scenarios, which gave the whole family considerably more confidence heading into 2026.

What to Do Now If You Rely on Medicaid Waiver Programs for In-Home Care

If your family currently depends on Medicaid waivers for in-home care, this is not the moment to assume the program will look the same in two years. A practical action list I recommend reviewing right now:

Confirm your current waiver enrollment status and annual renewal date with the Missouri Department of Social ServicesFamily Support Division

Ask your caseworker whether your specific waiver program is subject to enrollment caps or waiting lists under current state budget projections

Review your countable assets and income to understand where you stand against Missouri Medicaid eligibility thresholds today

Consult an elder law attorney to explore whether an irrevocable trust or other asset protection strategy should be in place before any coverage disruption occurs

Document all care being provided at home, including informal family caregiving, in case a caregiver child exemption or similar protection becomes relevant later

Medicaid enrollment figures can shift quickly under new federal rules, and the families who respond early are the ones with the most options.

Married Couples Face a Separate Set of Rules That Most People Never Read Until It’s Too Late

The Snapshot Date Missouri Uses to Calculate Your Countable Assets

Missouri Medicaid uses what is called a snapshot date, which is the first day of the first month a spouse enters a hospital or long-term care facility for a continuous stay that leads to a Medicaid application. On that specific date, Missouri calculates the total combined countable assets of both spouses, regardless of whose name they are in. That combined figure becomes the baseline from which the Community Spouse Resource Allowance of $162,660 is calculated. Most couples have no idea this snapshot moment exists until they are already past it.

How to Protect the Community Spouse’s Income When It Falls Below $2,644 Per Month

Missouri’s spousal impoverishment rules include an income protection floor for the spouse remaining at home, called the Monthly Maintenance Needs Allowance. In 2026, that floor is $2,644 per month. If the community spouse’s own income falls below that amount, Missouri allows a portion of the institutionalized spouse’s income to be redirected to the community spouse to close the gap. I have worked with couples where the wife’s only income was a small Social Security check, and this protection made the difference between genuine financial stability and real hardship.

A couple in their mid-seventies had spent decades building a small farming operation together. Nearly every asset was jointly titled, from the land to the equipment to the bank accounts. When the husband suffered a stroke requiring nursing home placement, the family assumed the jointly titled assets were somehow protected or split automatically. They were not. Missouri counted every jointly held dollar on the snapshot date. Fortunately, they came in early enough that we could still apply the full Community Spouse Resource Allowance and structure the remaining assets to minimize the spend-down requirement significantly.

Why Joint Assets Are Counted Differently Than Separate Assets During the Application

During a Missouri Medicaid application for a married couple, the Family Support Division counts all countable assets belonging to either spouse, regardless of how they are titled. A savings account in only the community spouse’s name is still counted. A brokerage account titled solely to the nursing home spouse is counted.

What changes is not whether the asset is counted, but how the Community Spouse Resource Allowance and spousal impoverishment standards are applied afterward to determine how much the community spouse gets to keep. Separate titling matters far less than most families assume, which is exactly why asset protection strategies need to be in place well before the application process begins.

The Law Offices of Christopher W. Dumm Protects Missouri and Arkansas Families From Nursing Home Costs

What 27 Years of Multi-State Elder Law Experience Gets You That a General Practice Attorney Cannot

Missouri Medicaid planning in 2026 is genuinely specialized work. The asset limits, transfer penalty divisors, estate recovery rules, spousal impoverishment standards, and Qualified Income Trust requirements across Missouri, Kansas, Arkansas, and Texas differ enough that a general practice attorney simply cannot carry this knowledge reliably.

I have been doing this since 1997, I teach it as an adjunct professor at Missouri Southern State University, and I am a member of WealthCounsel, ElderCounsel, and the National Academy of Elder Law Attorneys. That combination of courtroom experience and classroom depth is what your family deserves when this much is at stake.

Why Families in Joplin, Springfield, and Bentonville Keep Coming Back for Multiple Generations

The most honest thing I can tell you is that our clients stay because they trust us, and they trust us because we have never treated them like a transaction. We have clients who signed their first trust documents with us in 1999 and whose adult children are now sitting across from us planning their own estates. You are known by your name here, not a number. One client told us working with our office felt more like talking to a pastor than hiring a lawyer, and after 27 years, that still means more to us than any rating ever could.

How the LIFE Program Keeps Your Medicaid Plan Current as Laws and Asset Limits Change Each Year

Missouri Medicaid asset limits, transfer penalty divisors, and spousal impoverishment standards change every single year. A plan built in 2022 may have meaningful gaps by 2026 without a review. OurLIFE Program provides ongoing estate plan maintenance, educational workshops, and regular updates so your Medicaid asset protection strategy evolves as the rules and your life change. Estate planning is not a one-time event. It is a relationship, and we are committed to that relationship for as long as your family needs us.

Frequently Asked Questions

1. What is the Missouri Medicaid asset limit for a single applicant in 2026?

The Missouri Medicaid asset limit for a single nursing home applicant is $6,068.80, effective July 1, 2025. Most countable assets above that threshold must be spent down before MO HealthNet coverage begins.

2. How do spend-down strategies work under Missouri’s Spend Down Program?

Legal Medicaid spend-down strategies include paying off debt, making home modifications, and prepaying funeral expenses. The Family Support Division reviews asset verification systems carefully, so every spend-down transaction needs clean documentation to avoid triggering transfer penalties.

3. What is the difference between MAGI applications and non-MAGI applications in Missouri?

MAGI applications use income-based eligibility rules tied to the federal poverty line and cover groups like children and Medicaid expansion adults. Non-MAGI applications apply to seniors and people with disabilities seeking long-term care benefits, where both income and asset limits are evaluated separately.

4. What does Missouri Medicaid cover under MO HealthNet Covered Services for nursing home residents?

MO HealthNet covered services for nursing home residents include room and board, skilled nursing care, physician visits, prescription drugs, and therapy services. Coverage through a Managed Care Health Plan may vary slightly depending on which plan a recipient is enrolled in.

5. How does the Aged Blind and Disabled Non Spenddown pathway differ from the Medically Needy Pathway?

The Aged Blind and Disabled Non Spenddown program covers applicants whose income and assets fall within Missouri’s standard limits without requiring a spend-down calculation. The Medically Needy Pathway serves those whose income exceeds the limit but who can spend down medical expenses to qualify under Regular Medicaid rules.

6. What is House Joint Resolution 154 and how could it affect Missouri Medicaid recipients?

House Joint Resolution 154, sponsored by Rep. Darin Chappell of Rogersville and passed by the Missouri House of Representatives 99 to 48, proposes a Missouri Medicaidwork requirement amendment to the Missouri Constitution. If the Missouri State Senate passes it, Missouri voters will decide on November 3, 2026 whether to embed 80-hour monthly work requirements into the Missouri Constitution as a legislatively referred constitutional amendment.

7. Can a Life Estate Deed protect my home from Missouri Medicaid estate recovery?

A Life Estate Deed keeps you in the home during your lifetime while passing ownership to a named beneficiary at death, but Missouri’s estate recovery rules around Probate vs. Non-Probate recovery are broad enough to reach certain life estate arrangements. An irrevocable Medicaid Asset Protection Trust generally provides stronger and more reliable protection for most Missouri families.

8. What are Qualified Spousal Trusts and how do they fit into Missouri Medicaid Asset Protection planning?

Qualified Spousal Trusts are irrevocable trust structures designed to protect assets for the community spouse while removing them from countable resources for Medicaid eligibility purposes. They are one of several advanced Missouri Medicaid asset protection tools that work alongside spousal protections like the Community Spouse Resource Allowance.

9. Does Supplemental Security Income affect Missouri Medicaid eligibility for seniors?

Supplemental Security Income recipients are generally automatically eligible for MO HealthNet under the Aged Blind and Disabled pathways without a separate application. However, seniors with income above the SSI threshold may still qualify through the Medically Needy Pathway or spend-down strategies depending on their specific circumstances.

10. How do annual renewals work for Missouri Medicaid recipients after the public health emergency unwinding?

Following the end of pandemic-era continuous enrollment protections, Missouri Medicaid recipients must now complete annual renewals through the Family Support Division to maintain coverage. Missing renewal deadlines, even for procedural reasons, can result in coverage loss, so tracking renewal dates and responding promptly to MO HealthNet correspondence is genuinely important for every enrolled family.

Conclusion

Missouri Medicaid planning in 2026 rewards the families who act before a crisis forces their hand. The rules are specific, the deadlines are real, and the cost of waiting shows up in nursing home bills and estate recovery claims that erase what took decades to build. Our team has spent 27 years helping Missouri and Arkansas families protect exactly that. Every family’s situation is different, and yours deserves a personalized plan built around your specific assets, your state, and your timeline.

Schedule Your Free Consultation Today.